Financial Accounting Libby 9th Edition Solutions Chapter 9

Create your free account to read unlimited documents.

Jawaban chapter 9 adaptasi

![]()

You are reading a preview.

Create your free account to continue reading.

1

1

Like this document? Why not share!

- 4 Likes

- Statistics

- Notes

Jawaban chapter 9 adaptasi

- 1. CHAPTER 9 CONSOLIDATION OWNERSHIP ISSUES ANSWERS TO QUESTIONS Q9-1 Preferred stock of the subsidiary is eliminated in the consolidation process in a manner comparable to that used in eliminating the common stock of the subsidiary. For those preferred shares held by the parent company, a proportionate share of subsidiary income and net assets assigned to the preferred shares is eliminated against the balance in the parent's investment account. Subsidiary income and net assets assigned to preferred shares not held by the parent are included as a part of the noncontrolling interest along with the balances assigned to noncontrolling interest for common stock not held by the parent. The claim of the preferred shareholders normally is computed before the common stock is eliminated so that any priority claim associated with the preferred stock can be properly recognized and assigned to the correct shareholder group. Q9-2 All preferred shares held by the parent are eliminated against the balance in the investment account. Those held by unrelated parties are included in the total assigned to the noncontrolling interest. Q9-3 Preferred dividends normally are deducted in arriving at income available to common shareholders. When preferred dividends are paid by the subsidiary to shareholders other than the parent, the income accruing to the common shares held by the parent company is reduced. Therefore, they must be deducted to arrive at income available to the parent company shareholders. No preferred dividends are deducted if the parent company owns all the shares or if no dividends are declared and the preferred stock is noncumulative. Q9-4 In the event the preferred shares are redeemed, the subsidiary must pay the call premium and the net assets of the subsidiary will be reduced by the amount of the premium. Because it is more conservative to assume the call premium will be paid, the amount of the premium normally is added to the claim of the preferred shareholders and deducted from the equity assigned to the common shareholders whenever consolidated statements are prepared. Q9-5 The fair value of the net assets of the subsidiary is computed by deducting the fair value of the subsidiary's liabilities from the fair value of its assets. When the subsidiary has preferred stock outstanding, the claims of the preferred shareholders, including dividends in arrears and participation rights held by preferred shareholders, must be taken into consideration in determining the fair value of net assets available to common shareholders. These items, when deducted from the fair value of the identifiable assets of the acquired company, will reduce the amount of net assets assigned to common stock. In those cases where the purchase price of the common stock is not reduced proportionately, the amount assigned to goodwill will increase when the common stock is eliminated. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9- 1

- 2. Chapter 9 Q9-6 Under normal circumstances the parent will record a gain or loss on the difference between the carrying value of the shares sold and the sale price. For consolidation purposes the most appropriate treatment is to consider the point of sale to a nonaffiliate as the date of issue of the subsidiary shares. Any gain or loss recorded by the parent should be eliminated in the consolidation process and treated as a part of additional paid-in capital of the consolidated entity. Q9-7 All common shareholders should share equally in the net assets of a company. When a subsidiary sells additional shares to a nonaffiliate at a price in excess of existing book value, the effect will be to increase the net book value of all shareholders. Because it is a capital transaction, no gain or loss is recognized on the sale. Q9-8 Each purchase of additional shares should be examined to determine the difference between the price paid and underlying book value. When Rp10 over book value is paid for the shares, the parent will need to allocate that amount to either identifiable net assets or goodwill at the time the investment balance is eliminated and consolidated statements are prepared. Q9-9 All the shares of the subsidiary are eliminated in preparing the consolidated statements. Thus, treasury shares reported by the subsidiary are eliminated in the consolidation workpaper. The effect of the retirement on the consolidated statements depends on the price paid and whether the shares were purchased from the parent or from a nonaffiliate. Q9-10 Indirect ownership is a general term used whenever one company owns shares of another company and that company holds ownership in a third company. Indirect control occurs when a majority of the shares of a particular company are held by one or more companies that are, in turn, under the control of another company. By exercising its control over those companies the parent can exercise control of the company indirectly owned. Q9-11 A reciprocal relationship exists if Subsidiary A and Subsidiary B hold ownership in each other. If Subsidiary A records investment income based on the reported net income of Subsidiary B and Subsidiary B records investment income based on the reported net income of Subsidiary A, the sum of the reported net income totals for the two companies may be substantially greater than the sum of the reported operating income totals for the two companies. Parent company net income will be overstated if the impact of the reciprocal relationship is ignored when the parent company records investment income on its ownership in the two subsidiaries. Q9-12 Under the treasury stock method the parent company shares that have been purchased by a subsidiary are reported as treasury stock in the consolidated balance sheet. The carrying value of the shares is the amount paid by the subsidiary when they were purchased. Q9-13 The entity method focuses on the reciprocal nature of the ownership between the two companies. Income attributed to each company is computed by solving a set of simultaneous equations. Consolidated net income is then computed by multiplying the income computed for the parent by the percentage of ownership held by nonaffiliates. The treasury stock method is more simply applied, computing consolidated net income by deducting income assigned to noncontrolling shareholders from the combined operating incomes of the two companies in the normal manner. However, in this case, income assigned to the noncontrolling shareholders is based on the operating income of the subsidiary plus dividends received from the parent. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-2 Chapter 9

- 3. Q9-14 Consolidated net income will be reduced by Rp72,000 (Rp100,000 x .90 x .80) when the unrealized profit of Tiny Corporation is eliminated. A total of Rp10,000 is treated as a reduction to the income assigned to noncontrolling shareholders of Tiny Corporation (Rp100,000 x .10) and Rp18,000 is a reduction of the income assigned to noncontrolling shareholders of Subsidiary Company (Rp100,000 x .90 x .20). Q9-15 All three companies should be included in the consolidated financial statements. Slide Company should be consolidated with Bit Company because Bit holds majority ownership of Slide. Bit Company, in turn, should be consolidated with Snapper Corporation because Snapper holds majority ownership of Bit. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-3 Chapter 9 SOLUTIONS TO CASES

- 4. C9-1 Effect of Subsidiary Preferred Stock When a parent company owns all the outstanding preferred and common shares of its subsidiary, the contribution of the subsidiary to consolidated net income can be calculated on the basis of the reported net income of the subsidiary. In most cases the parent does not own all the shares of the subsidiary and income assigned to the noncontrolling interest includes (1) a portion of subsidiary preferred dividends and (2) a portion of earnings available to common shareholders. To determine the amount of income to assign to preferred and common shareholders of the subsidiary, the controller needs to have the following information about the preferred stock: 1. The number of preferred shares outstanding and the number owned by the parent and other affiliates. 2. The annual preferred dividend rate per share and whether the dividends are cumulative or noncumulative. 3. If the dividends are noncumulative, the amount of preferred dividends declared during the period, if any. In this particular case the parent does not appear to own any of the subsidiary's preferred shares. Once the controller determines the portion of subsidiary income assignable to common shareholders, consolidated net income is computed by adding the parent's pro rata share of this amount to the parent's income from its own operations. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-4 Chapter 9 C9-2 Presentation of Noncontrolling Interest MEMO To: Treasurer

- 5. PT Digdaya From: , Accounting Staff Re: PT Digdaya's Income on its Investment in PT Buana The consolidated financial statements prepared by PT Digdaya should include PT Buana. The purpose of consolidated financial statements is to present the financial position and results of operations for a parent and one or more subsidiaries as if the individual entities actually were a single company or entity. [ARB 51, Par 1] Consolidated income reported by PT Digdaya should include its share of the net income of PT Buana. However, the portion of PT Buana's net income assignable to its noncontrolling shareholders should not be included in Deep's reported net income. The correct amount of income to be reported by Deep in 20X4 from its investment in PT Buana is computed as follows: Common Preferred PT Buana's reported net income Rp200,000,000 Dividends to preferred shareholders (120,000,000) Rp120,000,000 Income to common shareholders Rp 80,000,000 Deep's ownership percentage .60 .10 Income to Deep Rp 48,000,000 Rp 12,000,000 While the company correctly reported dividend income of Rp12,000,000 from its investment in PT Buana's preferred stock, it should have reported only Rp48,000,000 (Rp80,000,000 x .60) of income on its investment in PT Buana's common stock instead of Rp120,000,000 (Rp200,000,000 x .60). This error has resulted in an overstatement of Deep's net income and its investment in PT Buana in the amount of Rp72,000,000 (Rp120,000,000 - Rp48,000,000). The appropriate corrections should be recorded by PT Digdaya and its financial statement revised, if already issued. If consolidated financial statements have already been issued and income of Rp140,000,000 [(Rp80,000,000 x .40) + (Rp120,000,000 x .90)] was not assigned to the noncontrolling shareholders, the income statement should be corrected and a corresponding adjustment made to the amount reported as noncontrolling interest in the consolidated balance sheet. Primary citation: ARB 51 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-5 Chapter 9 C9-3 Sale of Subsidiary Shares MEMO To: Robert Reader Vice President of Finance PT Barito

- 6. From: , CPA Re: Recognition of Gain on Sale of Subsidiary Shares Existing accounting standards do not specifically address the issue of recognizing a gain or loss on the sale of subsidiary shares when the parent retains controlling ownership. APB 18 deals explicitly with sales of stock of an investee, requiring recognition of a gain or loss on the difference between the selling price and carrying amount of the stock sold. [APB 18, Par. 19(f)] Equity-method reporting is intended to apply to those situations in which consolidation is not considered appropriate for financial reporting purposes. When the parent sells shares of the subsidiary but continues to hold controlling interest the issue of whether the gain or loss on the sale of shares should be carried to the consolidated income statement or eliminated in consolidation arises. The FASB suggested that no gain or loss be recognized. [FASB EXPOSURE DRAFT, "Consolidated Financial Statements, Including Accounting and Reporting of Noncontrolling Interests in Subsidiaries; a replacement of ARB No. 51," June 30, 2005, par. 23] In those situations where control is retained, it is proposed that the difference between the carrying value on the parent's PT Baritos before the sale and the sale price be recognized directly in equity (paid-in-capital). In current practice it is not uncommon for companies to report a gain when shares of a subsidiary are sold at more than carrying value and PT Barito would not appear to be in violation of current accounting procedures if it reports a gain of Rp48,000 in 20X1. However, the preferred method would be to report the Rp48,000 as additional paid-in capital. Primary citations: APB 18, Par. 19(f) FASB EXPOSURE DRAFT: CONSOLIDATED FINANCIAL STATEMENTS FASB PROJECT ON LIABILITIES AND EQUITIES Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-6 Chapter 9 C9-4 Sale of Subsidiary Shares A gain of Rp60 per share will be recorded by PT Himalaya on the sale to PT Bona regardless of whether the purchaser is an affiliate or a nonaffiliate. In both cases the gain must be eliminated in preparing the consolidated statements. (a) On a sale of shares to a nonaffiliate, net resources have been brought into the consolidated entity and there is an additional claim by the noncontrolling shareholders. It is considered appropriate to treat the gain recorded by the parent as an addition to consolidated additional paid-in capital in such cases. A sale of subsidiary shares to a nonaffiliate will also change the amount of income assigned to the noncontrolling interest in the consolidated

- 7. income statement and the amount of net assets assigned to noncontrolling interest in the consolidated balance sheet. (b) When a parent sells shares of one subsidiary to another subsidiary there is no increase in net resources to the consolidated entity, and the gain recorded by the parent must be eliminated when the investment balance reported by the subsidiary is eliminated. A change in the claim of the noncontrolling interest is likely to occur if the subsidiary that purchases the shares is not wholly-owned. As a result, there may be some change in consolidated income and the balance sheet totals assigned to noncontrolling interest. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-7 Chapter 9 C9-5 Reciprocal Ownership A great many factors beyond the immediate impact on reported earnings may be important in deciding on the use of the funds. Items such as the following should be considered: 1. Are the excess funds held by PT Tritani available only temporarily or not likely to be needed in the foreseeable future? 2. Will there be any regulatory or taxation problems associated with one or more of the alternatives? 3. Can shares of the companies be purchased in the desired quantities and at existing market prices or are there potential difficulties associated with one or more alternatives?

- 8. 4. Is it desirable to acquire more shares of either subsidiary since controlling ownership already is in the hands of Strong Manufacturing? 5. Have the noncontrolling shareholders of either subsidiary been troublesome or caused the parent to refrain from actions that it might otherwise have taken? With the information given, it is difficult to determine which action will have the most favorable impact on consolidated net income. The earnings of each company, the number of shares outstanding, and the relative market prices of the shares each will have an effect. In general, reported income is maximized by purchasing the shares with the lowest price-earnings ratio. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-8 Chapter 9 SOLUTIONS TO EXERCISES E9-1 Multiple-Choice Questions on Preferred Stock Ownership 1. d .20(Rp40,000,000 + Rp60,000,000) + 1.00(Rp30,000,000) = Rp50,000,000 2. c .20(Rp40,000,000 + Rp60,000,000) + .30(Rp30,000,000) = Rp29,000,000 3. b Only the retained earnings of the acquiring company is included. 4. a The portion held by the parent is eliminated when the preferred investment is eliminated, and the portion held by nonaffiliates is eliminated and included with the balance reported as noncontrolling interest in the consolidated balance sheet.

- 9. E9-2 Multiple-Choice Questions on Multilevel Ownership 1. b Rp100,000,000 + .80[Rp80,000,000 + .60(Rp50,000,000)] = Rp188,000,000 2. b .40(Rp50,000,000) = Rp20,000,000 3. c .20[Rp80,000,000 + .60(Rp50,000,000)] = Rp22,000,000 4. c .40(Rp50,000,000) + .20[Rp80,000,000 + .60(Rp50,000,000)] = Rp42,000,000 5. c .80[(Rp160,000,000 - Rp120,000,000) / 10 years] = Rp3,200,000 E9-3 Acquisition of Preferred Shares Eliminating entries: E(1) Common Stock — PT Sakura 50,000,000 Retained Earnings 150,000,000 Investment in PT Sakura Common Stock 140,000,000 Noncontrolling Interest 60,000,000 Eliminate investment in common stock. E(2) Preferred Stock — PT Sakura 100,000,000 Investment in PT Sakura Preferred Stock 60,000,000 Noncontrolling Interest 40,000,000 Eliminate subsidiary preferred stock. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9-9 Chapter 9 E9-4 Subsidiary with Preferred Stock Outstanding Eliminating entries: E(1) Common Stock — PT Tulip 150,000,000 Retained Earnings 210,000,000 Investment in PT Tulip Common Stock 270,000,000 Noncontrolling Interest 90,000,000 Eliminate investment in common stock. E(2) Preferred Stock — PT Tulip 200,000,000 Investment in PT Tulip Preferred Stock 80,000,000 Noncontrolling Interest 120,000,000 Eliminate subsidiary preferred stock. E9-5 Subsidiary with Preferred Stock Outstanding a. Entries recorded by Clayton Corporation:

- 10. (1) Investment in PT Tulip Common Stock 270,000,000 Investment in PT Tulip Preferred Stock 80,000,000 Cash 350,000,000 Record purchase of PT Tulip stock. (2) Cash 25,500,000 Investment in PT Tulip Common Stock 25,500,000 Record dividends from PT Tulip: Rp25,500,000 = (Rp50,000,000 - Rp16,000,000) x .75 (3) Cash 6,400,000 Dividend Income 6,400,000 Record dividends on preferred stock from PT Tulip: Rp16,000,000 x .40 (4) Investment in PT Tulip Common Stock 40,500,000 Income from Subsidiary 40,500,000 Record equity-method income: Rp40,500,000 = (Rp70,000,000 - Rp16,000,000) x .75 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 10 Chapter 9 E9-5 (continued) b. Eliminating entries: E(1) Income from Subsidiary 40,500,000 Dividends Declared — Common Stock 25,500,000 Investment in PT Tulip Common Stock 15,000,000 Eliminate income from subsidiary. E(2) Dividend Income — Preferred 6,400,000 Dividends Declared — Preferred 6,400,000 Eliminate dividend income from subsidiary preferred. E(3) Income to Noncontrolling Interest 23,100,000 Dividends Declared — Preferred Stock 9,600,000 Dividends Declared — Common Stock 8,500,000 Noncontrolling Interest 5,000,000 Assign income to noncontrolling interest: Rp23,100,000 = [(Rp70,000,000 - Rp16,000,000) x .25] + (Rp16,000,000 x .60) Rp9,600,000 = Rp16,000,000 x .60

- 11. Rp8,500,000 = (Rp50,000,000 - Rp16,000,000) x .25 Rp5,000,000 = Rp13,500,000 - Rp8,500,000 E(4) Common Stock — PT Tulip 150,000,000 Retained Earnings, January 1 210,000,000 Investment in PT Tulip Common Stock 270,000,000 Noncontrolling Interest 90,000,000 Eliminate beginning investment balance. E(5) Preferred Stock — PT Tulip 200,000,000 Investment in PT Tulip Preferred Stock 80,000,000 Noncontrolling Interest 120,000,000 Eliminate subsidiary preferred stock. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 11 Chapter 9 E9-6 Preferred Dividends and Call Premium a. PT Cempaka's contribution to 20X2 consolidated net income: Reported net income for 20X2 Rp70,000,000 Income assigned to noncontrolling interest: Preferred shares [.40(Rp100,000,000 x .12)] Rp4,800,000 Common shares {.10[Rp70,000,000 - 5,800,000 (10,600,000) (Rp100,000,000 x .12)]} Contribution to consolidated net income Rp59,400,000 b. Income assigned to the noncontrolling interest in 20X2, as computed in part (a), is Rp10,600,000. c. Retained earnings assignable to preferred shareholders: Dividends in arrears [5 years x (Rp100,000,000 x Rp60,000,000 .12)] Call feature (Rp2 x 10,000,000 shares) 20,000,000 Total retained earnings assigned to preferred Rp80,000,000 stock

- 12. d. Book value of common shares: Par value of common shares outstanding Rp300,000,000 Retained earnings balance Rp380,000,000 Less: Balance assigned to preferred shares (80,000,000) 300,000,000 Book value of common shares Rp600,000,000 e. Total noncontrolling interest: Preferred stock [.40(Rp100,000,000 + Rp 72,000,000 Rp80,000,000)] Common stock (.10 x Rp600,000,000) 60,000,000 Total noncontrolling interest Rp132,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 12 Chapter 9 E9-7 Multilevel Ownership a. Consolidated net income for 20X6 is Rp153,200: Operating income of PT Garuda Rp 90,000,000 Equity-method income from: Dally (Rp40,000,000 x .25) 10,000,000 Latent [(Rp60,000,000 + Rp16,000,000) x .70] 53,200,000 Consolidated net income Rp153,200,000 b. Income of Rp36,800,000 is assigned to noncontrolling interest: Income from Dally (Rp40,000,000 x .35) Rp14,000,000,000 Income from Latent [(Rp60,000,000 + Rp16,000,000) x .30] 22,800,000 Total income assigned Rp36,800 c. Only the Rp45,000,000 of dividends paid by PT Garuda to its shareholders will be reported as dividends declared in PT Garuda's 20X6 consolidated retained earnings statement.

- 13. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 13 Chapter 9 E9-8 Eliminating entries for Multilevel Ownership a. Journal entries recorded by PT Buana on its investment in PT Tarumanegara: (1) Investment in PT Tarumanegara Stock 120,000,000 Cash 120,000,000 Record purchase of PT Tarumanegara stock. (2) Cash 9,000,000 Investment in PT Tarumanegara Stock 9,000,000 Record dividends from PT Tarumanegara: Rp15,000,000 x .60 (3) Investment in PT Tarumanegara Stock 24,000,000 Income from PT Tarumanegara 24,000,000 Record equity-method income: Rp40,000,000 x .60 b. Journal entries recorded by PT Pandawa on its investment in PT Buana: (1) Investment in PT Buana Stock 315,000,000 Cash 315,000,000 Record purchase of PT Buana stock. (2) Cash 45,000,000 Investment in PT Buana Stock 45,000,000

- 14. Record dividends from PT Buana: Rp50,000,000 x .90 (3) Investment in PT Buana Stock 129,600,000 Income from PT Buana 129,600,000 Record equity-method income: (Rp120,000,000 + Rp24,000,000) x .90 c. Eliminating entries: E(1) Income from PT Tarumanegara 24,000,000 Dividends Declared 9,000,000 Investment in PT Tarumanegara Stock 15,000,000 Eliminate income from PT Tarumanegara. E(2) Income to Noncontrolling Interest 16,000,000 Dividends Declared 6,000,000 Noncontrolling Interest 10,000,000 Assign income to noncontrolling interest: Rp16,000,000 = Rp40,000,000 x .40 Rp6,000,000 = Rp15,000,000 x .40 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 14 Chapter 9 E9-9 (continued) E(3) Common Stock — PT Tarumanegara 100,000,000 Additional Paid-In Capital 60,000,000 Retained Earnings, January 1 40,000,000 Investment in PT Tarumanegara Stock 120,000,000 Noncontrolling Interest 80,000,000 Eliminate investment in PT Tarumanegara stock: Rp120,000,000 = Rp200,000,000 x .60 Rp80,000,000 = Rp200,000,000 x .40 E(4) Income from PT Buana 129,600,000 Dividends Declared 45,000,000 Investment in PT Buana Stock 84,600,000 Eliminate income from PT Buana. E(5) Income to Noncontrolling Interest 14,400,000 Dividends Declared 5,000,000 Noncontrolling Interest 9,400,000 Assign income to noncontrolling shareholders of PT Buana: Rp14,400,000 = (Rp120,000,000 + Rp24,000,000) x .10 Rp5,000,000 = Rp50,000,000 x .10 Rp9,400,000 = Rp14,400,000 - Rp5,000,000 E(6) Common Stock — PT Buana 150,000,000 Additional Paid-In Capital 60,000,000 Retained Earnings, January 1 140,000,000 Investment in PT Buana Stock 315,000,000 Noncontrolling Interest 35,000,000

- 15. Eliminate investment in PT Buana Corporation stock: Rp315,000,000 = Rp350,000,000 x .90 Rp35,000,000 = Rp350,000,000 x .10 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 15 Chapter 9 E9-9 Subsidiary Stock Dividend a. PT Lazuardi: Stock Dividends Declared 40,000,000 Common Stock 40,000,000 PT Laksmi: No entry required. b. Eliminating entries, December 31, 20X3: E(1) Income from Subsidiary 17,500,000 Dividends Declared 7,000,000 Investment in PT Lazuardi Stock 10,500,000 E(2) Income to Noncontrolling Interest 7,500,000 Dividends Declared 3,000,000 Noncontrolling Interest 4,500,000 E(3) Common Stock — PT Lazuardi 140,000,000 Retained Earnings, January 1 200,000,000 Investment in PT Lazuardi Stock 210,000,000 Noncontrolling Interest 90,000,000 Stock Dividends Declared 40,000,000 c. Eliminating entry, January 1, 20X4: E(1) Common Stock — PT Lazuardi 140,000,000 Retained Earnings 175,000,000 Investment in PT Lazuardi Stock 220,500,000 Noncontrolling Interest 94,500,000 PT Lazuardi retained earnings, December 31, 20X3:

- 16. Balance, December 31, 20X2 Rp200,000,000 Add: Net income for 20X3 25,000,000 Less: Stock dividend in 20X3 (40,000,000) Cash dividend paid in 20X3 (10,000,000) Balance, December 31, 20X3 Rp175,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 16 Chapter 9 E9-10 Sale of Subsidiary Shares by Parent a. Investment in PT Arjuna, January 1, 20X3: Purchase price Rp360,000,000 PT Arjuna net income in 20X3 and 20X4 Rp100,000,000 Dividends paid by PT Arjuna in 20X3 and 20X4 (40,000,000) Rp 60,000,000 Proportion of stock held by PT Sumo x .80 48,000,000 Balance prior to sale of shares Rp408,000,000 b. Journal entry recorded by PT Sumos for sale of shares: Cash 120,000,000 Investment in PT Arjuna Stock 102,000,000 Gain on Sale of PT Arjuna Stock 18,000,000 Rp102,000,000 = Rp408,000,000 x 4,000 / [(Rp200,000,000 / Rp10,000) x .80] c. Eliminating entries: E(1) Income from Subsidiary 30,000,000 Dividends Declared 12,000,000 Investment in PT Arjuna Stock 18,000,000 E(2) Income to Noncontrolling Interest 20,000,000 Dividends Declared 8,000,000 Noncontrolling Interest 12,000,000 E(3) Common Stock — PT Arjuna 200,000,000 Retained Earnings, January 1 310,000,000 Investment in PT Arjuna Stock 306,000,000 Noncontrolling interest 204,000,000 E(4) Gain on sale of PT Arjuna Stock 18,000,000 Additional Paid-In Capital 18,000,000

- 17. E9-11 Purchase of Additional Shares from Nonaffiliate a. Purchase price, December 31, 20X7 Rp240,000,000 PT Melati net income for 20X8 (Rp230,000,000 + Rp20,000,000 - Rp50,000,000 Rp200,000,000) Proportion of stock held by PT Widuri x .60 Rp30,000,000 Amortization of differential (Rp30,000,000 / 10 (3,000,000) years) Income from subsidiary 27,000,000 Dividends received from PT Melati (Rp20,000,000 x .60) (12,000,000) Balance in investment account, December 31, Rp255,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 17 Chapter 9 20X8

- 18. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 18 Chapter 9 E9-11 (continued) b. Balance in investment account, December 31, 20X8 Rp255,000,000 Purchase of additional shares on January 1, 20X9 96,000,000 PT Melati net income for 20X9 (Rp280,000,000 + Rp20,000,000 - Rp230,000,000) Rp70,000,000 Proportion of stock held by PT Widuri x .80 Rp56,000,000 Less: Amortization of differential on stock purchased: December 31, 20X7 (Rp30,000,000 / 10 years) (3,000,000) January 1, 20X9 (Rp20,000,000 / 10 years) (2,000,000) Income from subsidiary 51,000,000 Dividends received from PT Melati Company (Rp20,000,000 x .80) (16,000,000) Balance in investment account, December 31, 20X9 Rp386,000,000 c. Eliminating entries: E(1) Income from PT Melati 51,000,000 Dividends Declared 16,000,000 Investment in PT Melati Stock 35,000,000 E(2) Income to Noncontrolling Interest 14,000,000 Dividends Declared 4,000,000 Noncontrolling Interest 10,000,000 Rp14,000,000 = Rp70,000,000 x .20 E(3) Common Stock — PT Melati 150,000,000 Retained Earnings, January 1 230,000,000 Differential 47,000,000 Investment in PT Melati Company Stock 351,000,000 Noncontrolling Interest 76,000,000 Rp30,000,00 Differential on shares purchased, 0 December 31, 20X7 (3,000,00) Amortized in 20X8

- 19. Rp27,000,00 Unamortized balance 0 Differential on shares purchased, 20,000,000 January 1, 20X9 Unamortized purchase differential, Rp47,000,00 January 1, 20X9 0 E(4) Patents 42,000,000 Amortization Expense 5,000,000 Differential 47,000,000 Rp42,000,000 = (Rp47,000,000 - Rp3,000,000 - Rp2,000,000) Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 19 Chapter 9 E9-12 Repurchase of Shares by Subsidiary from Nonaffiliate a. Book value of PT Krisna stock outstanding Rp500,000,000 Cost of treasury shares repurchased (84,000,000) Book value of remaining shares outstanding Rp416,000,000 Proportion of remaining shares held by PT Brahmana (6,000 / 8,000) x .75 Adjusted book value of shares held by PT Brahmana Rp312,000,000 Book value of shares held by PT Brahmana before treasury stock repurchase by PT Krisna (Rp500,000,000 x .60) (300,000,000) Increase in carrying value of shares held by PT Brahmana Rp 12,000,000 b. Investment in PT Krisna Manufacturing Stock 12,000,000 Additional Paid-In Capital 12,000,000 c. Common Stock — PT Krisna Manufacturing 100,000,000 Additional Paid-In Capital 150,000,000 Retained Earnings, January 1 250,000,000 Investment in PT Krisna Stock 312,000,000 Noncontrolling Interest 104,000,000 Treasury Shares 84,000,000 Rp312,000,000 = .75(Rp500,000,000 - Rp84,000,000) Rp104,000,000 = .25(Rp500,000,000 - Rp84,000,000)

- 20. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 20 Chapter 9 E9-13 Sale of Shares by Subsidiary to Nonaffiliate a. Computation of change in book value of PT Sadewa shares held by PT Bhakti Yuda: Before After Sale Sale Common stock, Rp10,000 par value Rp150,000,000 Rp 200,000,000 Additional paid-in capital 50,000,000 400,000,000 Retained earnings 400,000,000 400,000,000 Total stockholders' equity of PT Sadewa Rp600,000,000 Rp1,000,000,000 Proportion of stock held by PT Bhakti Yuda Corporation: 11,000 / 15,000 x .733 11,000 / (15,000 + 5,000) x .550 Book value of shares Rp440,000,000 Rp 550,000,000 Increase in book value of shares held by PT Bhakti Yuda Rp 110,000,000 b. Investment in PT Sadewa Stock 110,000,000 Additional Paid-In Capital 110,000,000 c. Common Stock — PT Sadewa 200,000,000 Additional Paid-In Capital 400,000,000 Retained Earnings 400,000,000 Investment in PT Sadewa Stock 550,000,000 Noncontrolling Interest 450,000,000 Rp450,000,000 = Rp1,000,000,000 x .45

- 21. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 21 Chapter 9 SOLUTIONS TO PROBLEMS P9-14 Multiple-Choice Questions on Preferred Stock Ownership 1. d Book value of shares held by noncontrolling interest: Preferred stock (Rp100,000,000 x .30) Rp30,000,000 Common stock [(Rp200,000,000 + Rp50,000,000) x .20] 50,000,000 Total book value Rp80,000,000 2. b Income to noncontrolling preferred shareholders [(Rp100,000,000 x .10) x .30] Rp3,000,000 Income to noncontrolling common shareholders: Reported net income of PT Udayana Rp30,000,000 Income to preferred shareholders (10,000,000) Income to common shareholders Rp20,000,000 Proportion of common stock owned by noncontrolling interest x .20 4,000,000 Total income to noncontrolling interest Rp7,000,000 3. b Reported net income of PT Udayana Rp 30,000,000 Operating income of PT Srikandi 100,000,000 Rp130,000,000 Less: Income to noncontrolling interest (7,000,000) Consolidated net income Rp123,000,000 4. a Parent company balance at date of acquisition. 5. a All preferred shares of the subsidiary are eliminated in preparing the consolidated financial statements.

- 22. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 22 Chapter 9 P9-15 Multilevel Ownership with Purchase Differential a. Journal entries recorded by PT Cahaya on its investment in PT Bina Jaya: (1) Investment in PT Bina Jaya Stock 405,000,000 Cash 405,000,000 Record purchase of PT Bina Jaya stock. (2) Cash 14,000,000 Investment in PT Bina Jaya Stock 14,000,000 Record dividends from PT Bina Jaya: Rp20,000,000 x .70 (3) Investment in PT Bina Jaya Stock 21,000,000 Income from PT Bina Jaya 21,000,000 Record equity-method income: Rp30,000,000 x .70 (4) Income from PT Bina Jaya 2,000,000 Investment in PT Bina Jaya Stock 2,000,000 Amortize differential related to buildings and equipment: Rp20,000,000 / 10 years b. Journal entries recorded by PT Permata on its investment in PT Cahaya: (1) Cash 20,000,000 Investment in PT Cahaya Stock 20,000,000 Record dividends from PT Cahaya: Rp25,000,000 x .80 (2) Investment in PT Cahaya Stock 63,200,000 Income from PT Cahaya 63,200,000 Record equity-method income: (Rp60,000,000 + Rp19,000,000) x .80 (3) Income from PT Cahaya 8,000,000 Investment in PT Cahaya Stock 8,000,000 Amortize differential related to trademark: Rp40,000,000 / 5 years

- 23. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 23 Chapter 9 P9-15 (continued) c. Eliminating entries: E(1) Income from PT Bina Jaya 19,000 Dividends Declared 14,000 Investment in PT Bina Jaya Stock 5,000 Eliminate income from PT Bina Jaya. E(2) Income to Noncontrolling Interest 9,000 Dividends Declared 6,000 Noncontrolling Interest 3,000 Assign income to noncontrolling shareholders of PT Bina Jaya: Rp9,000 = Rp30,000 x .30 Rp6,000 = Rp20,000 x .30 Rp3,000 = Rp9,000 - Rp6,000 E(3) Common Stock — PT Bina Jaya 250,000 Retained Earnings, January 1 300,000 Differential 20,000 Investment in PT Bina Jaya Stock 405,000 Noncontrolling Interest 165,000 Eliminate investment in PT Bina Jaya stock: Rp20,000 = Rp405,000 - (Rp550,000 x .70) Rp405,000 = Purchase price Rp165,000 = Rp550,000 x .30 E(4) Buildings and Equipment 20,000 Differential 20,000 Assign beginning differential. E(5) Depreciation Expense 2,000 Accumulated Depreciation 2,000 Amortize differential related to buildings and equipment: Rp20,000 / 10 years E(6) Income from PT Cahaya 55,200 Dividends Declared 20,000 Investment in PT Cahaya Stock 35,200 Eliminate income from PT Cahaya. E(7) Income to Noncontrolling Interest 15,800 Dividends Declared 5,000 Noncontrolling Interest 10,800 Assign income to noncontrolling shareholders of PT Cahaya: Rp15,800 = (Rp60,000 + Rp19,000) x .20 Rp5,000 = Rp25,000 x .20 Rp10,800 = Rp15,800 - Rp5,000

- 24. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 24 Chapter 9 P9-18 (continued) E(8) Common Stock — PT Cahaya 400,000,000 Retained Earnings, January 1 270,000,000 Differential 24,000,000 Investment in PT Cahaya Stock 560,000,000 Noncontrolling Interest 134,000,000 Eliminate investment in PT Cahaya stock: Rp270,000,000 = Rp200,000,000 + Rp35,000,000 + Rp35,000,000 Rp24,000,000 = Rp40,000,000 - Rp8,000,000 - Rp8,000,000 Rp560,000,000 = Rp520,000,000 + [(Rp60,000,000 - Rp25,000,000) x .80 - Rp8,000,000] x 2 years Rp134,000,000 = (Rp400,000,000 + Rp270,000,000) x .20 E(9) Trademark 24,000,000 Differential 24,000,000 Assign beginning differential: Rp40,000,000 - (Rp8,000,000 x 2 years) E(10) Amortization Expense 8,000,000 Trademark 8,000,000 Amortize differential related to trademark: Rp40,000,000 / 5 years Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 25

- 25. Chapter 9 P9-16 Subsidiary Stock Dividend Investment elimination entry, January 1, 20X8: Alternative 1: PT Prima Perkasa stock is split 2:1. E(1) Common Stock — PT Prima Perkasa 100,000,000 Additional Paid-In Capital 70,000,000 Retained Earnings 280,000,000 Investment in PT Prima Perkasa Stock 306,000,000 Noncontrolling Interest 144,000,000 Alternative 2: A stock dividend of 4,000 shares is issued. E(1) Common Stock — PT Prima Perkasa 140,000,000 Additional Paid-In Capital 70,000,000 Retained Earnings 240,000,000 Investment in PT Prima Perkasa Stock 306,000,000 Noncontrolling Interest 144,000,000 Alternative 3: A stock dividend of 1,500 shares is issued. E(1) Common Stock — PT Prima Perkasa 115,000,000 Additional Paid-In Capital 130,000,000 Retained Earnings 205,000,000 Investment in PT Prima Perkasa Stock 306,000,000 Noncontrolling Interest 144,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 26

- 26. Chapter 9 P9-17 Subsidiary Preferred Stock Outstanding a. Eliminating entries, January 1, 20X5: Preferred Stock — PT Prabu 200,000,000 Retained Earnings 32,000,000 Investment in PT Prabu Preferred Stock 92,800,000 Noncontrolling Interest 139,200,000 Eliminate preferred stock: Rp32,000,000 = (Rp200,000,000 x .08) x 2 years Common Stock — PT Prabu 150,000,000 Retained Earnings 168,000,000 Investment in PT Prabu Common Stock 222,600,000 Noncontrolling Interest 95,400,000 Eliminate common stock: Rp168,000,000 = Rp200,000,000 - Rp32,000,000 b. Consolidated net income: Operating income of PT Erlangga Rp80,000,000 Income from preferred stock of PT Prabu (Rp16,000,000 x .40) 6,400,000 Income from common stock of PT Prabu [(Rp34,000,000 - Rp16,000,000) x .70] 12,600,000 Consolidated net income Rp99,000,000 Income to noncontrolling interest: Income from preferred stock of PT Prabu (Rp16,000,000 x .60) Rp 9,600,000 Income from common stock of PT Prabu [(Rp34,000,000 - Rp16,000,000) x .30] 5,400,000 Income to noncontrolling shareholders Rp15,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 27 Chapter 9

- 27. P9-18 Ownership of Subsidiary Preferred Stock a. Preferred stockholders' claim on net assets of PT Jayakarta: Liquidation value of preferred stock (Rp101 per share) Rp202,000,000 20X6 dividends in arrears (Rp200,000,000 x .10) 20,000,000 Total preferred stockholder claim, December 31, 20X6 Rp222,000,000 b. Book value of PT Jayakarta common shares purchased by PT Pelita: Total PT Jayakarta stockholders' equity, December 31, 20X6 Rp3,155,000,000 Claim of preferred stockholders (222,000,000) Book value of PT Jayakarta common stock Rp2,933,000,000 Portion acquired by PT Pelita x .60 Book value of common shares purchased by PT Pelita Rp1,759,800,000 c. Goodwill associated with purchase of common shares: Purchase price of common shares Rp1,800,000,000 Book value of common shares purchased (1,759,800,000) Goodwill Rp 40,200,000 d. Income to noncontrolling interest, 20X7: PT Jayakarta net income Rp280,000,000 Less: 20X7 preferred dividends (Rp200,000 x .10) (20,000,000) Income accruing to common shareholders Rp260,000,000 Noncontrolling common shareholders' interest x .40 Income to noncontrolling common shareholders Rp104,000,000 Preferred dividends to noncontrolling shareholders (Rp20,000,000 x .80) 16,000,000 Total income to noncontrolling shareholders Rp120,000,000 e. PT Pelita's income from investment in subsidiary common stock: PT Jayakarta net income Rp280,000,000 Less: 20X7 preferred dividends (Rp200,000,000 x .10) (20,000,000) Income accruing to common shareholders Rp260,000,000 PT Pelita's proportionate share x .60 PT Pelita's share of income to common shareholders Rp156,000,000 f. Noncontrolling interest, December 31, 20X7: PT Jayakarta stockholders' equity, January 1, 20X7 Rp3,155,000,000 20X7 net income 280,000,000 Less: Preferred dividends (40,000,000) Less: Common dividends (10,000,000) Total PT Jayakarta stockholders' equity, December 31, 20X7 Rp3,385,000,000 Claim of preferred stockholders (202,000,000) Book value of PT Jayakarta' common stock Rp3,183,000,000 Noncontrolling stockholders' interest x .40 Noncontrolling interest — common Rp1,273,200,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 28 Chapter 9 P9-18 (continued)

- 28. Total PT Jayakarta preferred stockholders' equity, January 1, 20X7 Rp222,000,000 Less: Dividends in arrears paid during 20X7 (20,000,000) PT Jayakarta preferred stockholders' equity, December 31, 20X7 Rp202,000,000 Noncontrolling stockholders' interest x .80 Noncontrolling interest — preferred Rp161,600,000 Noncontrolling interest — common Rp1,273,200,000 Noncontrolling interest — preferred 161,600,000 Total noncontrolling interest Rp1,434,800,000 g. Eliminating entries: E(1) Income from Subsidiary 156,000,000 Dividends Declared — Common 6,000,000 Investment in PT Jayakarta Common Stock 150,000,000 Eliminate income from subsidiary. E(2) Dividend Income — Preferred 8,000,000 Dividends Declared — Preferred 8,000,000 Eliminate dividend income from subsidiary preferred stock: Rp40,000,000 x .20 E(3) Income to Noncontrolling Interest 120,000,000 Dividends Declared — Common 4,000,000 Dividends Declared — Preferred 32,000,000 Noncontrolling Interest 84,000,000 Assign income to noncontrolling interest: Rp4,000,000 = Rp10,000,000 x .40 Rp32,000,000 = Rp40,000,000 x .80 E(4) Common Stock — PT Jayakarta Jacuzzi 500,000,000 Additional Paid-In Capital — Common 800,000,000 Premium on Preferred Stock 3,000,000 * Retained Earnings, January 1 1,630,000,000 ** Goodwill 40,200,000 Investment in PT Jayakarta Common Stock 1,800,000,000 Noncontrolling Interest 1,173,200,000 Eliminate beginning investment in common stock: Rp3,000,000 = Rp5,000,000 - Rp2,000,000 Rp1,630,000,000 = Rp1,650,000,000 - Rp20,000,000 Rp1,173,200,000 = (Rp500,000,000 + Rp800,000,000 + Rp3,000,000 + Rp1,630,000,000) x .40 *Portion accruing to common shareholders **Portion accruing to common shareholders after deducting preferred dividends in arrears Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 29 Chapter 9 P9-18 (continued) E(5) Goodwill Impairment Loss 26,000,000 Goodwill 26,000,000 Recognize goodwill impairment loss.

- 29. E(6) Preferred Stock — PT Jayakarta 200,000,000 Premium on Preferred Stock 2,000,000 * Retained Earnings, January 1 20,000,000 ** Investment in Jacobs Preferred Stock 42,000,000 Additional Paid-In Capital — Retirement of Preferred Stock 2,400,000 Noncontrolling Interest 177,600,000 Eliminate subsidiary preferred stock: Rp2,000,000 = Rp5,000,000 - Rp3,000,000 Rp20,000,000 = Rp200,000,000 x .10 Rp2,400,000 = (Rp222,000,000 x .20) - Rp42,000,000 Rp177,600,000 = Rp222,000,000 x .8 *Portion representing call premium **Portion relating to preferred dividends in arrears P9-19 Consolidation Workpaper with Subsidiary Preferred Stock a. Eliminating entries: E(1) Income from Subsidiary 58,500,000 Dividends Declared — Common Stock 9,000,000 Investment in PT Wijaya Kusuma Common 49,500,000 Stock E(2) Dividend Income 9,000,000 Dividends Declared — Preferred Stock 9,000,000 E(3) Income to Noncontrolling Interest 12,500,000 Dividends Declared — Preferred Stock 6,000,000 Dividends Declared — Common Stock 1,000,000 Noncontrolling Interest 5,500,000 E(4) Common Stock — PT Wijaya Kusuma 100,000,000 Corporation Retained Earnings, January 1 250,000,000 Investment in PT Wijaya Kusuma Common Stock 315,000,000 Noncontrolling Interest 35,000,000 E(5) Preferred Stock — PT Wijaya Kusuma 200,000,000 Corporation Investment in PT Wijaya Kusuma Preferred Stock 120,000,000 Noncontrolling Interest 80,000,000 E(6) Dividends Payable 9,000,000 Dividends Receivable 9,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 30 Chapter 9 P9-19 (continued) b. PT Buana and PT Wijaya Kusuma Consolidation Workpaper December 31, 20X6

- 30. PT Wijaya PT Buana Kusuma Eliminations Consol- Item ________ __________ Debit Credit idated Sales 500,000,000 300,000,000 800,000,000 Dividend Income 9,000,000 (2) 9,000,000 Income from 58,500,000 (1) 58,500,000 Subsidiary Credits 567,500,000 300,000,000 800,000,000 Cost of Goods Sold 280,000,000 170,000,000 450,000,000 Deprec. and Amort. 40,000,000 30,000,000 70,000,000 Other Expenses 131,000,000 20,000,000 151,000,000 Debits (451,000,000) (220,000,000) (671,000,000) Income to Noncon- 129,000,000 trolling Interest (3) 12,500,000 (12,500,000) Net Income, carry forward 116,500,000 80,000,000 80,000,000 116,500,000 Retained Earnings, 435,000,000 250,000,000 (4) 250,000,000 435,000,000 Jan. 1 Net Income, from 116,500,000 80,000,000 80,000,000 116,500,000 above 551,500,000 330,000,000 551,500,000 Dividends Declared Preferred Stock (15,000,000) (2) 9,000,000 (3) 6,000,000 Common Stock (60,000,000) (10,000,000) (1) 9,000,000 (3) 1,000,000 (60,000,000) Ret. Earnings, Dec. 31, carry forward 491,500,000 305,000,000 330,000,000 25,000,000 491,500,000 Cash 58,000,000 100,000,000 158,000,000 Accounts Receivable 80,000,000 120,000,000 200,000,000 Dividends Receivable 9,000,000 (6) 9,000,000 Inventory 100,000,000 200,000,000 300,000,000 Bldgs. and Equip. (net) 360,000,000 270,000,000 630,000,000 Investment in PT Wijaya Kusuma: Preferred Stock 120,000,000 (5) 120,000,000 Common Stock 364,500,000 (1) 49,500,000 (4) 315,000,000 Debits 1,091,500,000 690,000,000 1,288,000,000 Accounts Payable 100,000,000 70,000,000 170,000,000 Dividends Payable 15,000,000 (6) 9,000,000 6,000,000 Bonds Payable 300,000,000 300,000,000 Preferred Stock (5) 200,000,000 200,000,000 Common Stock 200,000,000 100,000,000 (4) 100,000,000 200,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 31 Chapter 9 Ret. Earnings, from 491,500,000 305,000,000 330,000,000 25,000,000 491,500,000

- 31. above Noncontrolling Interest (3) 5,500,000 (4) 35,000,000 (5) 80,000,000 120,500,000 Credits 1,091,500,000 690,000,000 639,000,000 639,000,000 1,288,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 32 Chapter 9 P9-20 Subsidiary Stock Transactions a. (1) Book value of PT Brajamusti stock outstanding Rp500,000,000 Cost of treasury shares repurchased (68,000,000)

- 32. Book value of remaining shares Rp432,000,000 outstanding Proportion of remaining shares held by PT Andalas (7,500 / 9,000) x .833 Adjusted book value of shares held by PT Rp360,000,000 Andalas Book value of shares held by PT Andalas before treasury stock repurchase by PT Brajamusti (Rp500,000,000 x .75) 375,000,000 Decrease in carrying value of shares held by PT Andalas Rp (15,000,000) (2) Journal entry recorded by PT Andalas Corporation: Retained Earnings 15,000,000 Investment in PT Brajamusti Stock 15,000,000 (3) Eliminating entries: E(1) Income from Subsidiary 37,500,000 Investment in PT Brajamusti Stock 37,500,000 Rp45,000,000 x .833 E(2) Income to Noncontrolling Interest 7,500,000 Noncontrolling Interest 7,500,000 Rp45,000,000 x .167 E(3) Common Stock — PT Brajamusti 100,000,000 Additional Paid-In Capital 80,000,000 Retained Earnings, January 1 320,000,000 Treasury Stock 68,000,000 Investment in PT Brajamusti Stock 360,000,000 Noncontrolling Interest 72,000,000 b. (1) Book value of PT Brajamusti stock outstanding Rp500,000,000 Cost of treasury shares repurchased (68,000,000) Book value of remaining shares outstanding Rp432,000,000 Proportion of remaining shares held by PT Andalas (6,500 / 9,000) x .722 Adjusted book value of shares held by PT Andalas Rp312,000,000 Book value of shares held by PT Andalas before treasury stock repurchase by PT Brajamusti (Rp500,000,000 x .75) (375,000,000) Change in carrying value of shares held by PT Andalas Rp (63,000,000) (2) Journal entry recorded by PT Andalas Corporation: Cash 68,000,000 Investment in PT Brajamusti Stock 63,000,000 Gain on Sale of Investment 5,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 33 Chapter 9 P9-20 (continued) (3) Eliminating entries: E(1) Gain on Sale of Investment 5,000,000

- 33. Additional Paid-In Capital 5,000,000 E(2) Income from Subsidiary 32,500,000 Investment in PT Brajamusti Stock 32,500,000 Rp45,000,000 x .722 E(3) Income to Noncontrolling Interest 12,500,000 Noncontrolling Interest 12,500,000 Rp45,000,000 x .278 E(4) Common Stock — PT Brajamusti 100,000,000 Additional Paid-In Capital 80,000,000 Retained Earnings, January 1 320,000,000 Treasury Stock 68,000,000 Investment in PT Brajamusti Stock 312,000,000 Noncontrolling Interest 120,000,000 P9-21 Sale of Subsidiary Shares a. Eliminating entries: E(1) Gain on Sale of PT Eka Karya Stock 10,000,000 Additional Paid-In Capital 10,000,000 Eliminate gain on sale of PT Eka Karya shares: Rp60,000,000 - (Rp250,000,000 x .20) E(2) Income from Subsidiary 18,000,000 Dividends Declared 6,000,000 Investment in PT Eka Karya Stock 12,000,000 Eliminate income from subsidiary: Rp18,000,000 = .60(Rp170,000,000 - Rp140,000,000) E(3) Income to Noncontrolling Interest 12,000,000 Dividends Declared 4,000,000 Noncontrolling Interest 8,000,000 Assign income to noncontrolling interest: Rp12,000,000 = .40(Rp170,000,000 - Rp140,000,000) E(4) Common Stock — PT Eka Karya 100,000,000 Additional Paid-In Capital 20,000,000 Retained Earnings, January 1 130,000,000 Investment in PT Eka Karya Stock 150,000,000 Noncontrolling Interest 100,000,000 Eliminate investment in common stock. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 34 Chapter 9 P9-21 (continued) b. PT Pronto and PT Eka Karya Consolidation Workpaper December 31, 20X4 PT Eka Karya PT Pronto

- 34. Eliminations Consol- Item ______ _______ Debit Credit idated Sales 280,000,000 170,000,000 450,000,000 Gain on Sale of PT Eka Karya Company Stock 10,000,000 (1) 10,000,000 Income from Subsidiary 18,000,000 _______ (2) 18,000,000 Credits 308,000,000 170,000,000 450,000,000 Cost of Goods Sold 210,000,000 100,000,000 310,000,000 Depreciation Expense 20,000,000 15,000,000 35,000,000 Other Expenses 21,000,000 25,000,000 46,000,000 Debits (251,000,000) (140,000,000) (391,000,000) 59,000,000 Income to Noncon- trolling Interest (3) 12,000,000 (12,000,000) Net Income, carry forward 57,000,000 30,000,000 40,000,000 47,000,000 Retained Earnings, January 1 320,000,000 130,000,000 (4)130,000,000 320,000,000 Net Income, from above 57,000,000 30,000,000 40,000,000 47,000,000 377,000,000 160,000,000 367,000,000 Dividends Declared (15,000,000) (10,000,000) (2) 6,000,000 (3) 4,000,000 (15,000,000) Ret. Earnings, Dec. 31, carry forward 150,000,000 170,000,000 10,000,000 352,000,000 362,000,000 Cash 30,000,000 35,000,000 65,000,000 Accounts Receivable 70,000,000 50,000,000 120,000,000 Inventory 120,000,000 100,000,000 220,000,000 Buildings and Equipment 650,000,000 230,000,000 880,000,000 Investment in PT Eka Karya Company Stock 162,000,000 (2) 12,000,000 (4) 150,000,000 Debits 1,032,000,000 415,000,000 1,285,000,000 Accum. Depreciation 170,000,000 95,000,000 265,000,000 Accounts Payable 50,000,000 20,000,000 70,000,000 Bonds Payable 200,000,000 30,000,000 230,000,000 Common Stock 200,000,000 100,000,000 (4)100,000,000 200,000,000 Additional Paid-In Capital 50,000,000 20,000,000 (4) 20,000,000 (1) 10,000,000 60,000,000 Retained Earnings, from above 362,000,000 150,000,000 170,000,000 10,000,000 352,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 35 Chapter 9 Noncontrolling Interest (3) 8,000,000 (4)100,000,000 108,000,000 Credits 1,032,000,000 415,000,000 290,000,000 290,000,000 1,285,000,000

- 35. Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 36 Chapter 9 P9-21 Sale of Shares by Subsidiary to Nonaffiliate a. E(1) Common Stock — PT Dahlia 240,000,000 Additional Paid-In Capital 190,000,000 Retained Earnings 350,000,000 Investment in PT Dahlia Stock 520,000,000 Noncontrolling Interest 260,000,000 Eliminate investment in common stock: Rp240,000,000 = Rp200,000,000 + (Rp10,000 x 4,000 shares) Rp190,000,000 = Rp50,000,000 + [(Rp45,000 - Rp10,000) x 4,000 shares] Rp520,000,000 = Rp780,000,000 x (16,000 shares / 24,000 shares)

- 36. Rp260,000,000 = Rp780,000,000 x (8,000 shares / 24,000 shares) Journal entry recorded by PT Citra: Investment in PT Dahlia Stock 40,000,000 Additional Paid-In Capital 40,000,000 Book value of shares held by PT Citra: After sale Rp780,000,000 x (16,000 / 24,000) Rp520,000,000 Before sale Rp600,000,000 x (16,000 / 20,000) (480,000,000) Increase in book value Rp 40,000,000 b. PT Citra and PT Dahlia Consolidated Balance Sheet Workpaper January 1, 20X3 PT Citra PT Dahlia Eliminations Consol- Item ____ ____ Debit Credit idated Cash 50,000,000 230,000,000 280,000,000 Accounts Receivable 90,000,000 120,000,000 210,000,000 Inventory 180,000,000 200,000,000 380,000,000 Buildings & Equipment 700,000,000 600,000,000 1,300,000,000 Investment in PT Dahlia Corporation 520,000,000 (1)520,000,000 Total Debits 1,540,000,000 1,150,000,000 2,170,000,000 Accumulated Depreciation 200,000,000 220,000,000 420,000,000 Accounts Payable 70,000,000 70,000,000 140,000,000 Taxes Payable 80,000,000 80,000,000 Mortgages Payable 250,000,000 250,000,000 Common Stock 300,000,000 240,000,000 (1)240,000,000 300,000,000 Additional Paid-In Capital 220,000,000 190,000,000 (1)190,000,000 220,000,000 Retained Earnings, 500,000,000 350,000,000 (1)350,000,000 500,000,000 Noncontrolling Interest (1)260,000,000 260,000,000 Total Credits 1,540,000,000 1,150,000,000 780,000,000 780,000,000 2,170,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 37 Chapter 9 P9-25 (continued) c. PT Citra and Subsidiary Consolidated Balance Sheet January 1, 20X3 Current Assets: Cash Rp 280,000,000 Accounts Receivable 210,000,000 Inventory 380,000,000 Rp 870,000,000 Noncurrent Assets:

- 37. Buildings and Equipment Rp1,300,000,000 Less: Accumulated Depreciation (420,000,000) 880,000,000 Total Assets Rp1,750,000,000 Current Liabilities: Accounts Payable Rp 140,000,000 Taxes Payable 80,000,000 Rp 220,000,000 Mortgages Payable 250,000,000 Noncontrolling Interest 260,000,000 Stockholders' Equity: Common Stock Rp 300,000,000 Additional Paid-In Capital 220,000,000 Retained Earnings 500,000,000 1,020,000,000 Total Liabilities and Stockholders' Equity Rp1,750,000,000 Solutions Manual – Baker / Lembke / King / Jeffrey, Advanced Financial Accounting, 7e 9 - 38 Chapter 9 P9-26 Sale of Additional Shares to Parent a. Eliminating entry: E(1) Common Stock — PT Toronto 125,000,000 Additional Paid-In Capital 175,000,000 Retained Earnings 200,000,000 Buildings and Equipment 12,500,000 Investment in PT Toronto 412,500,000 Noncontrolling Interest 100,000,000 Journal entry recorded by PT Toronto: Cash 150,000,000 Common Stock 25,000,000 Additional Paid-In Capital 125,000,000

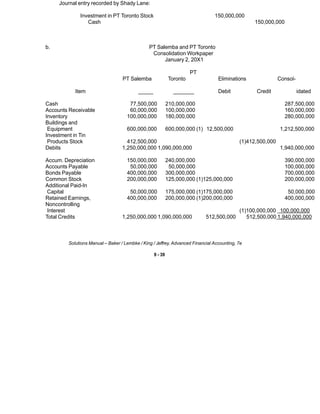

Financial Accounting Libby 9th Edition Solutions Chapter 9

Source: https://www.slideshare.net/rizzahim/jawaban-chapter-9-adaptasi